Innovative Debt Relief Strategies: Automation Unleashed

Debt relief encompasses strategies and services aimed at managing overwhelming debt burdens. With global consumer debt on the rise, there's a pressing need for innovative solutions.

Traditionally, debt relief involved tailored debt management plans by credit counseling services and formal debt consolidation programs. However, these methods often rely on outdated, manual processes that are slow and limited in scope.

Advancements in automation, powered by AI algorithms and machine learning, offer a transformative path forward. These technologies can swiftly analyze financial data to create personalized debt solutions. This article explores how forward-thinking debt relief providers are integrating automation to enhance their services.

The Potential of Automation in Debt Management

Automation is increasingly driving greater productivity, efficiency, and innovation across the financial services sector worldwide. In the specific domain of consumer debt management, AI algorithms, machine learning predictive models, and RPA software robots are taking on a multitude of repetitive, time-intensive manual work. This is helping to streamline operations for providers and assist you in regaining control of your precarious finances.

Debt relief strategies aim to manage overwhelming debt burdens, crucial as global consumer debt rises. Traditionally, solutions included tailored plans by credit counseling services and debt consolidation programs. Yet, these methods often rely on slow, manual processes.

Automation, driven by AI and machine learning, presents a transformative solution. These technologies analyze financial data swiftly, crafting personalized debt solutions. This article explores how innovative debt relief providers integrate automation to enhance their services.

Automated Budgeting and Payment Optimization

Conducting a thorough assessment of your financial situation is crucial for effective debt management. This process can be complex, especially for seniors who may find manual budgeting challenging. However, various resources are available to help individuals regain control over their finances. For example, residents exploring debt relief programs in Michigan can access both local and online options that offer guidance and tools for managing debts. These programs often utilize AI-powered FinTech tools that streamline personal budgeting by integrating with bank accounts and employing machine learning algorithms.

Such technologies can provide tailored budgeting recommendations and automate transaction categorization, making it easier for individuals of all ages to monitor their finances and work towards their debt relief goals.

Intelligent categorization – Machine learning classifiers can analyze raw transaction descriptions and automatically categorize them into common buckets like housing, food, transportation, utilities, and discretionary expenses. This provides a breakdown of where cash is being spent.

Anomaly detection – AI algorithms can further detect unusual spending activity and ratios that may be early indicators of financial stress, missed payments, or even fraud. This enables corrective actions.

Simulated scenarios – Leveraging aggregated income and spending data, AI tools can simulate different debt payment and budget scenarios across obligations. Models predict the probability of successfully adhering to each combination based on personalized financial constraints. The optimal payment schedule is recommended.

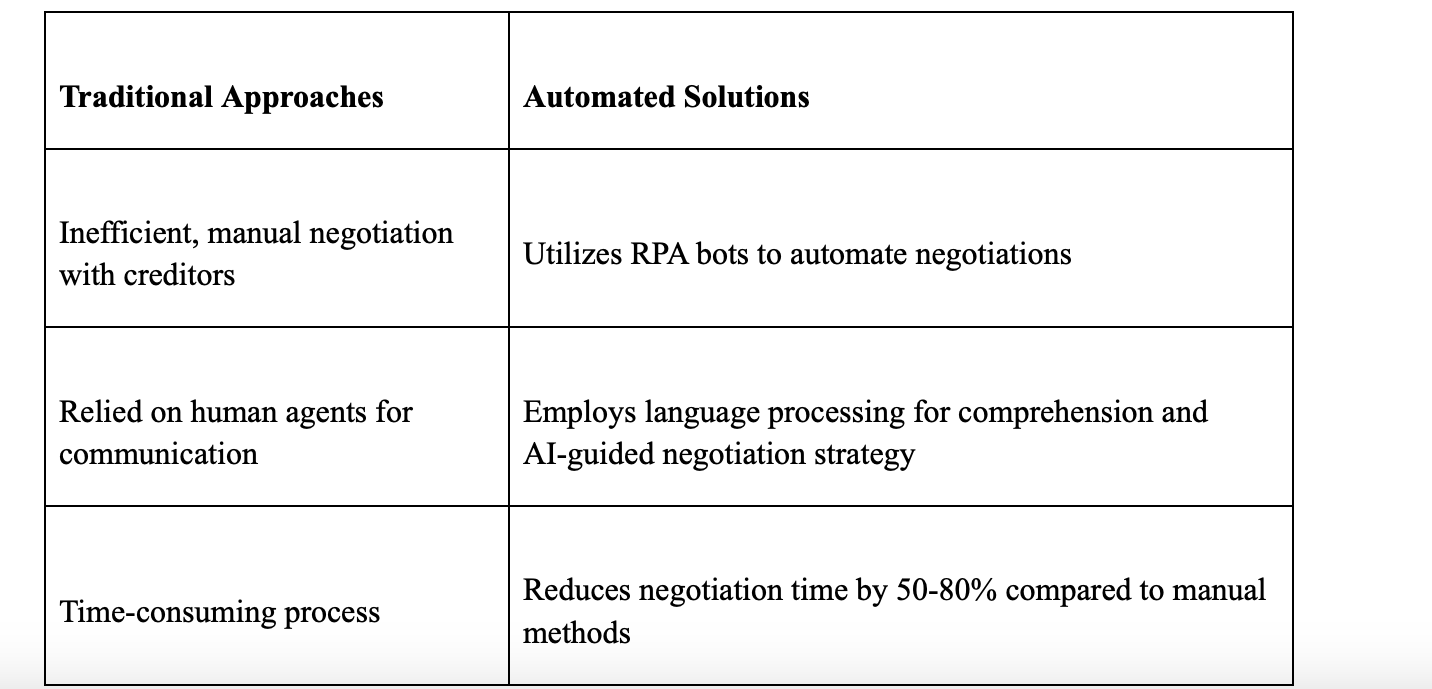

Robotic Process Automation for Streamlined Negotiations

Negotiating with multiple creditors and debt collection agencies to reduce interest rates or fees and establish more affordable payment terms has long been an inefficient, frustrating manual process for indebted consumers. The importance of money is undeniable in these situations, robotic process automation introduces the possibility for automated software bots to emulate these administrative conversations and interactions at far greater scale to accelerate debt relief outcomes.

Language processing for comprehension – RPA bots can be trained using machine learning techniques to interpret unstructured text from emails, call transcripts, and even scanned letters to extract salient details on outstanding debts like amounts owed, dates, account numbers, etc.

AI-guided negotiation strategy - Based on aggregated data on your obligations, advanced algorithms can determine negotiation priorities and sequence along with acceptable settlement terms and discounts to propose per debt based on empirically derived likelihood of creditor acceptance. This replaces guesswork.

Autonomous communication at scale – Leveraging libraries of optimized scripts and language processing, RPA bots can autonomously correspond with creditors and collectors through various channels including email, phone calls, and live chat simultaneously to execute negotiated terms and settlements. Human agents would be unable to match this relentless follow-up cadence.

According to research published in the Harvard Business Review, RPA automation can reduce the time required to complete key debt negotiation processes by 50-80% compared to manual methods, leading to expedited settlements and dramatically lowered costs for both you and providers. Further, automated bots consistently follow best practices and compliance rules to secure optimal terms.

Automation-Enabled Experiences: From Personalized Relief to Instant Support

While strategic priorities like operational efficiency and risk management are undoubtedly paramount, enhanced personalization of debt relief solutions alongside superior consumer experiences should be considered equally important objectives enabled by thoughtful automation.

Robotic Process Automation for Streamlined Negotiations

Tailored Debt Recommendations

Historically, many debt relief providers pursued a mostly one-size-fits-all approach relying on a few standardized solutions and creditor negotiation scripts which failed to address the nuanced challenges and diverse needs of different consumers. The advent of AI and machine learning introduces the capability to develop far more dynamic and tailored debt relief recommendations customized to your circumstances.

Predictive analytics - Debt assessment algorithms can analyze your financial profiles, obligations, and self-reported goals/concerns to predict the optimal solutions from a range of available debt management, consolidation, settlement, or counseling options. Success likelihood for each plan is quantified for transparency.

Continuous adaptation – Plan recommendations can be automatically fine-tuned based on your ongoing financial actions, risk profile changes, and macroeconomic trends to ensure sustained relevance rather than stagnation. Unexpected job loss or medical bills would trigger advice adjustments, for example.

Conversational interfaces – AI chatbots can engage you in free-form conversations regarding your financial priorities, concerns, and constraints. This subjective qualitative data augments technical analytics to further personalize debt payoff or settlement strategies. Human nuance is incorporated.

Safeguarding Your Data with Automation

Protecting your personal and financial information is an imperative, longstanding priority for financial institutions that becomes even more critical as debt management workflows shift to be data-driven. AI and machine learning systems must be engineered to embed privacy and compliance by design.

End-to-end encryption – All ingested consumer data within automated debt systems, including documents, statements, account details, payments, should be encrypted whether at rest in storage or in transit between internal applications to prevent unauthorized access in the event of breaches. State-of-the-art protocols like AES-256 should be implemented.

Access controls – Granular, role-based permission policies on a need-to-know basis should govern which human handlers and AI/ML models can access various data elements and for what predefined purposes. Analytics teams may see anonymized datasets only, for example.

Right to be forgotten – Your rights to request data deletion and systems compliance with regulations like GDPR and CCPA should be enabled by APIs that can automatically locate and permanently erase specific consumer information completely across all databases and logs.

Adhering to these strict security and compliance practices is essential for maintaining public trust as automation becomes further entrenched in debt management. Failing to do so poses major legal, financial, and reputational risks that could lead to existential crises, as evidenced by various data scandals.

Transparency and Explainability in Automated Decisions

Given the inherent complexity of modern artificial intelligence algorithms, enhanced transparency and explainability are required when machine learning models drive critical debt assessments and recommendations that substantially impact your finances and credit.

Local explanations – Providers should be able to clarify the key factors, data variables, and logic that influenced any given individual debt analysis or recommendation to demystify results and identify potential anomalies. This instills confidence.

Global model explainability – Broadly, the machine learning development process, selected training data, internal validation results, and performance metrics should be documented and open to audit to verify models are performing as intended without bias. Ethically questionable correlations can be discovered early and addressed.

Audit trails – Comprehensive activity and versioning logs that trace how automation tools arrived at each decision help to promote model accountability and trust. Records also aid debugging efforts.

Subjecting algorithms powering automated advising and negotiations to both internal and external scrutiny through comprehensive transparency practices can help uphold compliance with fair lending rules and appropriate consumer protections while averting AI misuse.

Delivering on Automation's Promise: Integration and Adoption Hurdles

To fully realize the immense potential of automation in debt relief, providers must thoughtfully tackle integration complexities stemming from legacy systems reliance alongside proactively addressing your perceptions.

Overcoming Technical Integration Barriers

The majority of established debt relief providers rely on a patchwork of dated manual processes, siloed datasets, and disjointed software tools built up over decades. Integrating new AI, machine learning, and RPA technologies with these heterogeneous technical environments can prove challenging.

Transition planning – Prior to automation rollouts, meticulous technical planning is required to catalog all necessary data preparation, migration, and system API integration needs to avoid critical oversights that cause failures. Staff training plans should also be completed.

Proactive preparation – Data pipelines need to be built, legacy data cleaned and formatted, and APIs or microservices established for core platforms well in advance of integrating automation tools to prevent delays. Adequate compute infrastructure provisioning also needs to occur.

Phased deployments – Given complex dependencies, a big bang launch is ill-advised. Rolling out automation capabilities incrementally by line of business allows for addressing inevitable configuration issues, optimization, and organizational change management before widespread adoption. This minimizes disruption.

Overcoming Your Misconceptions

Some debt-burdened consumers may doubt automated software’s ability to entirely replace human judgment and provide the necessary client empathy. As such, providers should market and position automation transparently to overcome misconceptions.

Building trust – Clear, non-technical explanations of how AI recommendations are derived and validated instill confidence in its reasoning abilities. Further, emphasizing human oversight roles in approving system actions promotes trust.

Clarifying generative capabilities – Conversational interfaces like chatbots should be framed as digital assistants that can augment specialists by handling routine inquiries, while seamlessly connecting you to empathetic counselors for complex needs. This demonstrates complementary value.

Promoting personalization – The ability to automatically analyze large datasets and client profiles to derive customized debt relief solutions should be conveyed to counter fears of impersonal, rigid automation. Humans simply lack this scale.

Proactively educating you on how AI and automation ultimately aim to enhance, not replace, human skills and relationships can lead to greater acceptance of inevitable technology shifts.

Future Automation Trajectory: Better Predictions, Better Outcomes

Intelligent automation will continue shaping the rapid evolution of the broader debt relief sector for the foreseeable future. Already emerging capabilities in predictive analytics, blockchain-based decentralized lending, and hybrid human-AI decision-making hint at a future defined by true partnerships between people and technology.

Predictive behavioral modeling – Increasingly sophisticated algorithms fed more expansive data will gain the ability to forecast major life events, income fluctuations, and spending shocks for you. These insights can trigger personalized and preemptive debt interventions before situations deteriorate.

Blockchain architectures – Distributed ledger technologies offer the possibility for frictionless consolidation of various consumer debt obligations across lending platforms into single blockchain loan instruments with immutable terms and smart contract facilitated payment automation.

Co-piloting hybrid models – Blending automation’s untiring processing capacities with human proficiency in emotional intelligence and subjective reasoning will produce higher fidelity insights than either people or AI could generate independently. This synthesis is critical for complex financial matters.

Driven by these innovations, the future trajectory points to you enjoying both optimized and more holistic debt management empowered by technology while retaining human oversight and wisdom.

FAQs

1. How secure are automated debt relief platforms in safeguarding my financial information?

Reputable providers implement robust encryption, access controls, and cybersecurity measures to protect consumer data within automated systems. Strict audits also ensure platforms align with regulations like GDPR and CCPA. Overall, automated systems can match or even exceed the data security levels of manual processes.

2. What is the role of human advisors in an automated debt relief platform?

Automation complements rather than replaces human expertise. Advisors supervise and enhance automated systems while focusing on relationship-building, complex financial planning, and providing emotional support during stressful situations.

3. Can AI chatbots fully replicate human conversations and emotional intelligence?

While rapidly advancing, today's AI still lacks the nuance and empathy of human interactions. Ethical providers position chatbots as digital assistants that connect consumers to human experts for complex conversations requiring discretion and emotional intelligence.

More Financial Articles